We want to keep you up to date on all things real estate! Preview of a brand-new communication that's being shared with Compass agents on a monthly basis, to you. It includes national-level data points around the real estate market, mortgage rates, and the broader economic environment that you can use. Let us know your thoughts and if you'd like me to share next month's updates or any of your real estate questions. Call Jack at (203) 253-0476 or reach the team by email [email protected].

Where Does Inflation Stand?

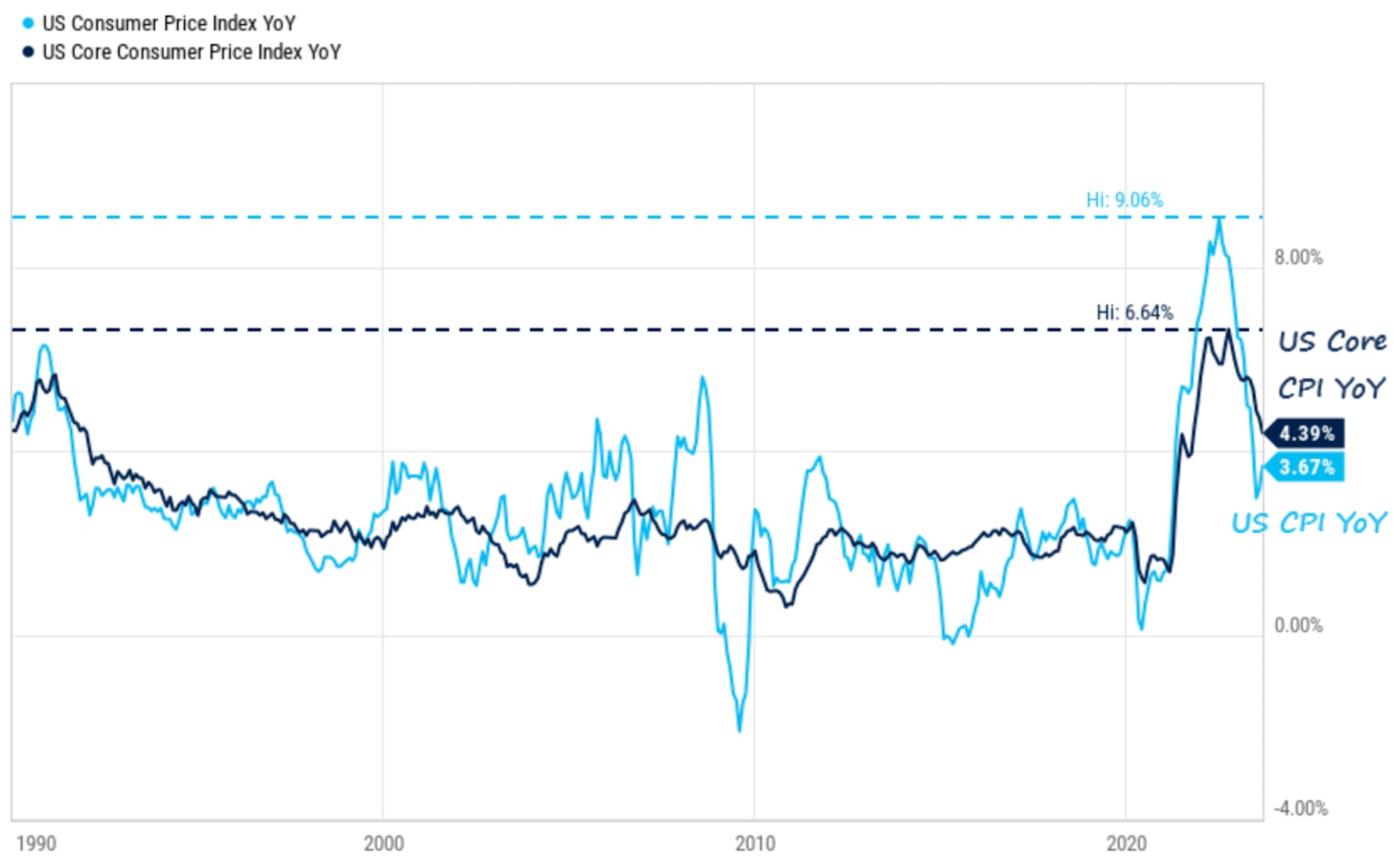

Earlier this week, we saw the most recent inflation numbers come out, showing overall US CPI moved up to 3.7% in August from 3.2% in July, the 2nd straight month with an increasing YoY inflation rate. While we would like to see inflation trending down, these small increases were expected given the increase in the price of retail gasoline and were not cause for concern. The core CPI, which removes food and energy from its measure (since those items tend to be volatile), increased 0.3% and 4.3% respectively. The Fed focuses more on core inflation as it provides a better indication of where inflation is heading over the long term.

US Core CPI (ex-Food/Energy) moved down to 4.3% YoY, the lowest core inflation reading since September 2021.

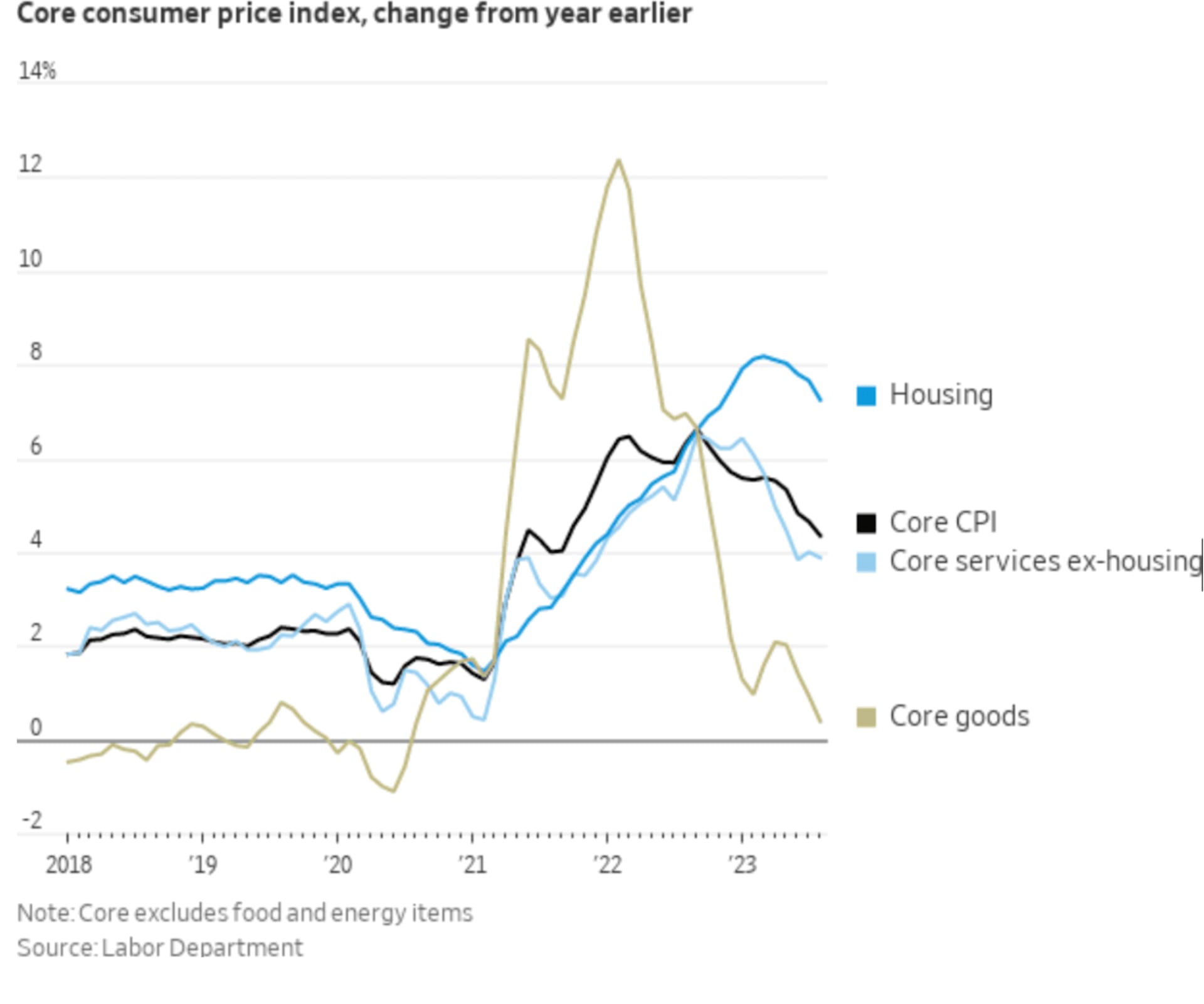

When looking at these numbers in a vacuum, it could be cause for concern. However, it's important to step back and look at what are the key components of CPI to get a sense if this is just a short term blip or a longer term trend. Housing makes up 30% of CPI so it has a massive impact on where it is and where it's going.

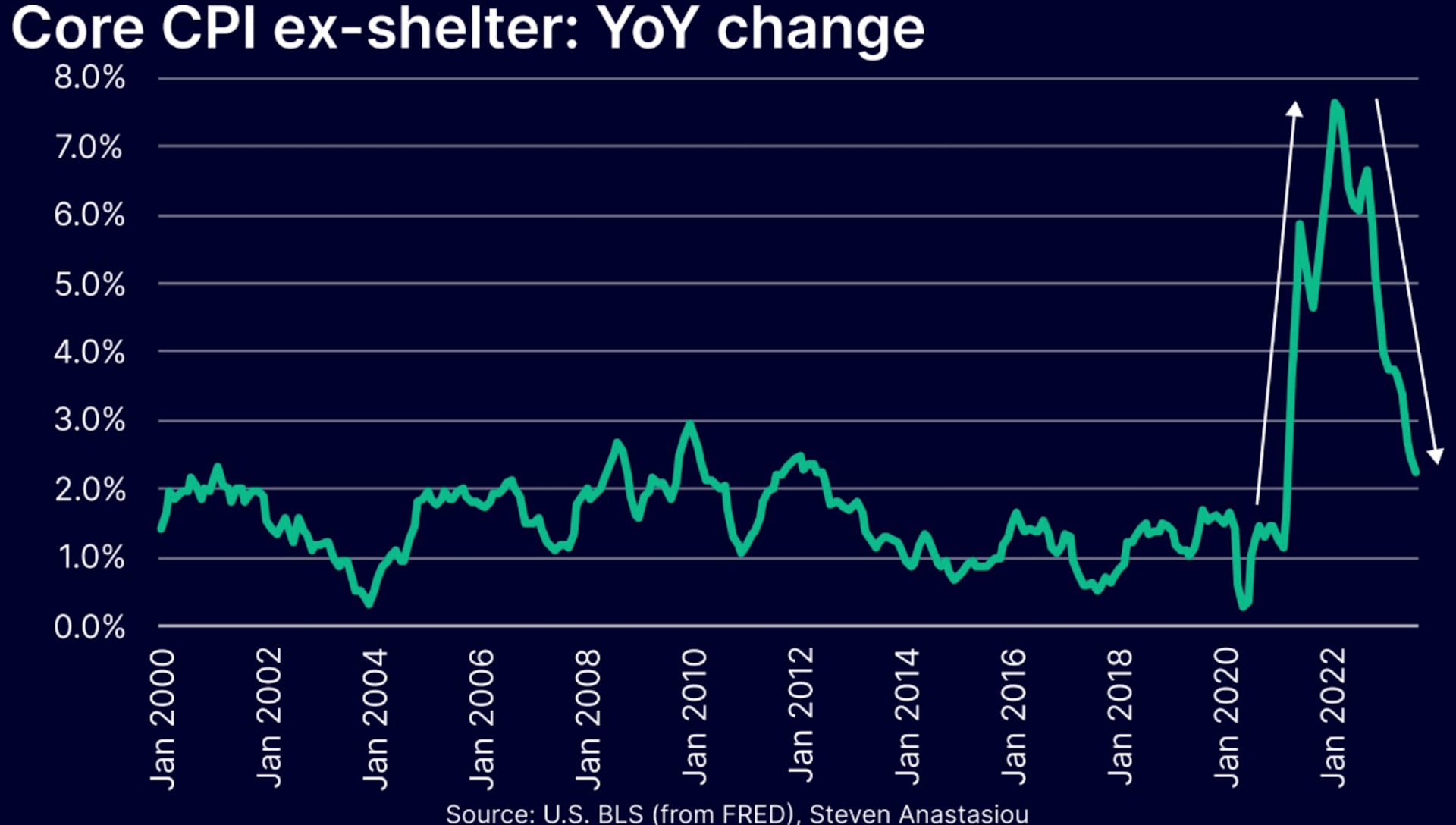

First, let's look at inflation without housing data. If you take lagging shelter measures out of the equation, the rest of the core CPI has decelerated to just 2.2% YoY. That is good news and shows that outside of housing inflation is coming down. Additionally, the supply of money has been declining over the last year. With less money in circulation many believe inflation will continue to fall.

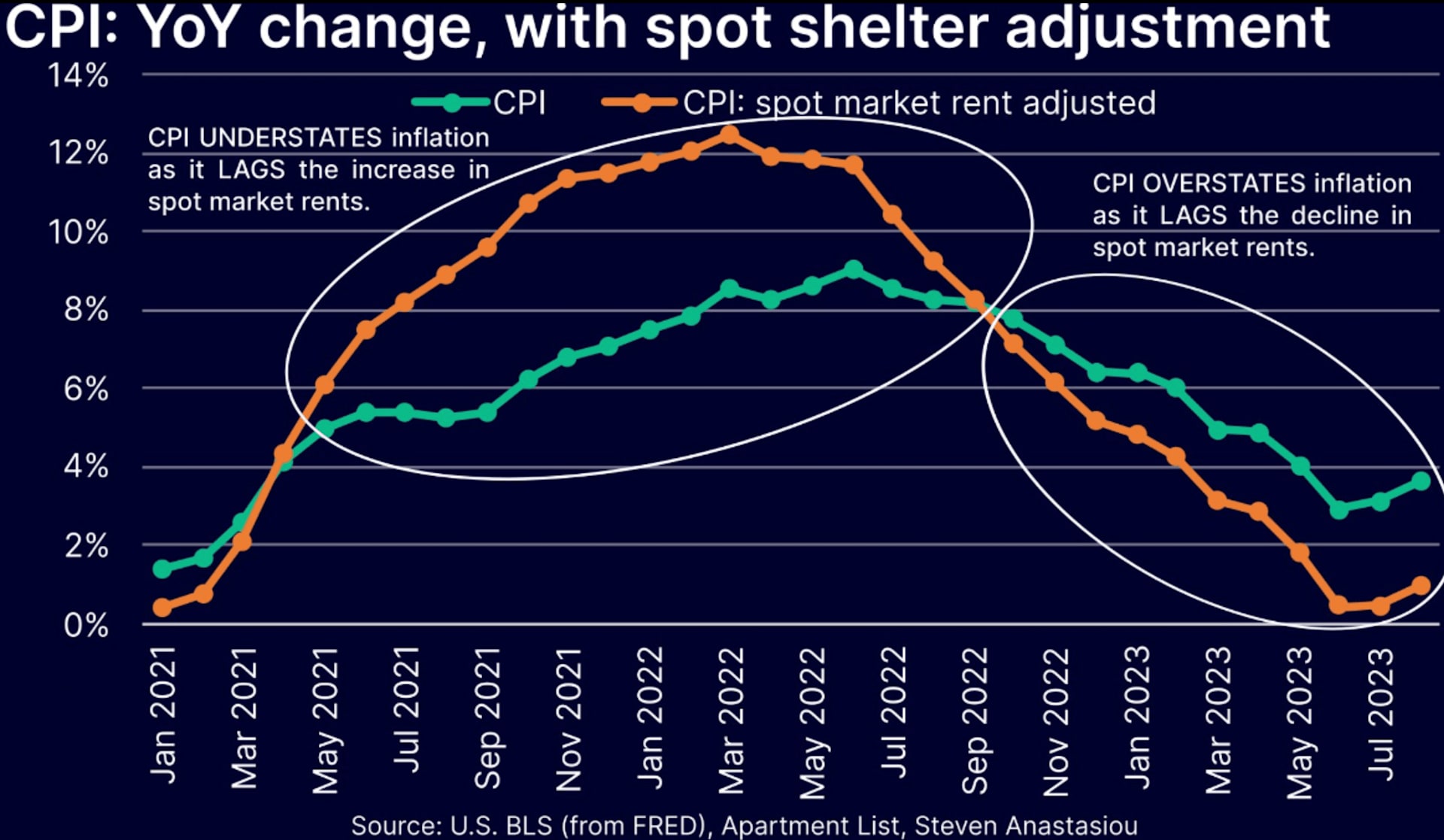

Looking now at inflation with housing and shelter information, let's include real time shelter data instead of the lagging data the Fed looks at. If we use real time rents, CPI growth is just 1.0% YoY, materially below the unadjusted rate of 3.7%.

By not adjusting the CPI's lagging rent based measures for spot (real time) market rents during times of large swings in rental prices, the numbers can be skewed. This is one of the reasons that many have called for the Fed to use real time housing data when looking at inflation measures.

Lastly, if we look at inflation in terms of goods inflation, we are almost back to where we were before the pandemic. However, housing is still delayed and therefore is likely a source of future disinflation. Should this trend continue, it will help bring CPI down and the Fed will consider their job done. At that point, the narrative will shift to rate cuts instead of rate increases. Here is to hoping this trend continues!